Carvana (CVNA) recently surprised the market – and us – when it reported its first-ever annual profit.

At LikeFolio, we’re great at predicting revenue. Our social media machine detects swings in consumer demand that lead us to winning trades.

(LikeFolio Investor subscribers just made a whopping 389% gain on one of those alerts. And we can show you the next big winner here.)

But the internal workings of a company are out of our range.

We weren’t expecting CVNA to go skyward like it did…

But we can take a retrospective look back to see what we can learn – and how we can best play CVNA from here.

Let’s start with the results:

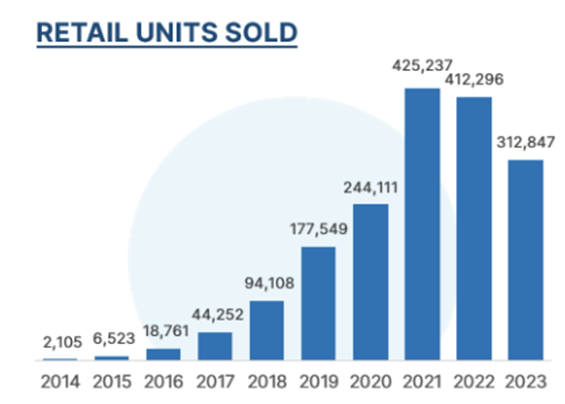

- Q4 Revenue: $2.42 billion (-13% YoY)

- Q4 Retail Units Sold: -6% YoY

- FY23 Net Income: $150 million

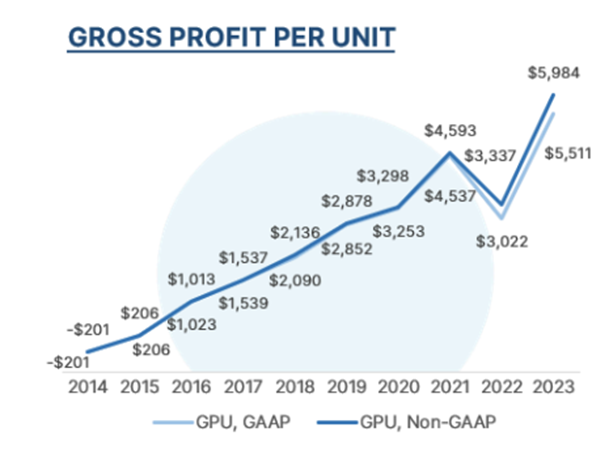

The third bullet – net income – is the major driver of investor optimism, assisted by Carvana’s ability to generate a larger gross profit per unit than the year prior.

You can see the stark turnaround in the images below:

Carvana achieved this massive feat by effectively leveraging technology and streamlining its own internal processes. This allowed the company to:

- Trim down the time its own employees spent per sale by 40%

- Lower the average days-to-sale by ~70 days (from its peak in 2023)

- Reduce the non-vehicle cost of a sale by $900 per unit

Whew.

The takeaway: Carvana and its team are getting better at moving and selling vehicles – so even though the total number of units sold did fall, operational improvements more than offset the weakness.

This ticks off Step 2 of Carvana’s three-step plan (driving fundamental gains in GPU and operational efficiency).

Step 3: Return to Growth

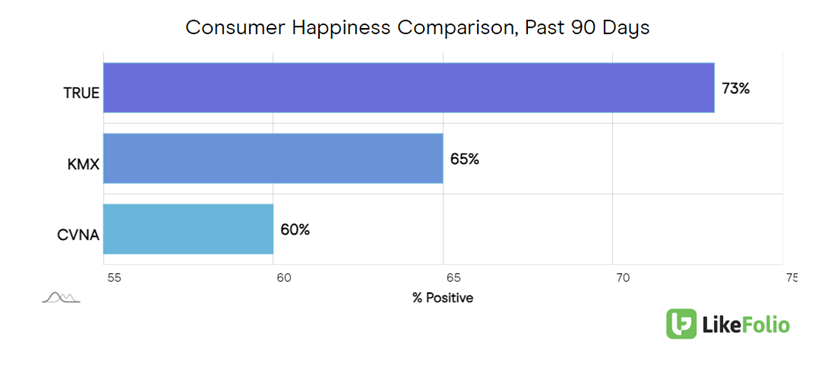

LikeFolio consumer data shows Carvana still has plenty of room for improvement.

Stacked up against other used vehicle peers, TrueCar (TRUE) and CarMax (KMX), it sits at the bottom of the pack in Consumer Happiness at just 60% positive:

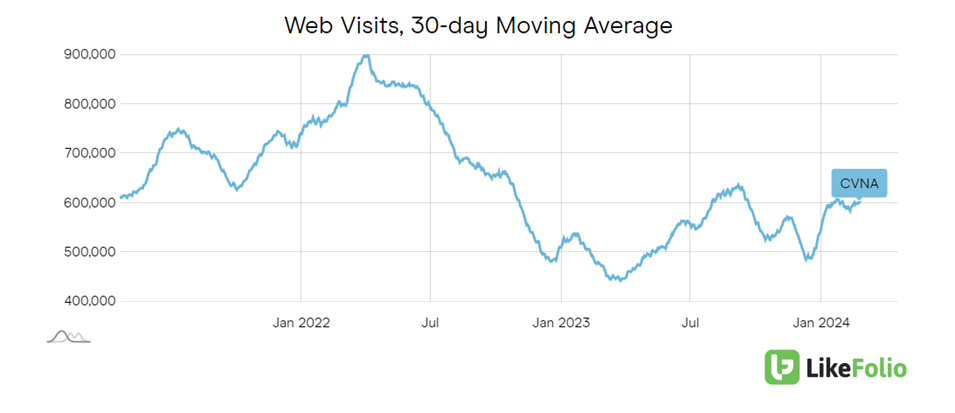

Web visits do show some near-term traction, up 15% year over year, but still nowhere near where it was a few years ago.

(On a two-year stack, visits are down 24%.)

💡 Assuming Carvana can maintain the operational efficiency it’s achieved, web visits will prove extremely valuable to watch to better understand how many cars are changing hands.

After a sequential dip in volume, has the company maxed out its profit squeeze?

We’ll see.

Carvana claims just 1% of a $1 trillion market, and demand does suggest some improvement in volume – an indicator of additional market share steal.

Even after gaining 750% over the last year, shares have plenty of room to catch up to their 2021 highs. The zoomed-out look puts things into perspective:

Bottom line: With a trillion-dollar market opportunity in front of it, Carvana has plenty of room to grow. We expect continued momentum in this name.

Until next time,

Andy Swan

Founder, LikeFolio

More Insights from Derby City Daily

Stay ahead of the investing curve with the latest consumer demand insights from Derby City Daily. Here’s what’s new…

NVDA Who? This AI Chip Maker Could Surge in 2024

Wall Street is still underestimating this name, but we see a massive opportunity…

You Don’t Need to Buy Bitcoin to Ride This Rally

This publicly-traded stock could be your ticket to DeFi profits…